Authors

In conversation with Vincent Mortier, Group CIO, Amundi

In this special edition of Amundi’s Newsletter for Central Banks, we sat down with Amundi’s Chief Investment Officer, Vincent Mortier, to explore the evolving market dynamics. From navigating geopolitical shifts to refining asset allocation strategies, he shares key perspectives on how to identify opportunities in a rapidly changing global landscape.

Welcome to the third edition of Amundi’s Newsletter for Central Banks, crafted by our experts for you.

In a complex macroeconomic and geopolitical environment, our specialists share their views on global policy and investment themes important to central banks worldwide.

In this edition, we explore the possibility of multi-speed growth and examine the investment outlook for the remainder of the year, including in emerging markets. We also analyse the impact of risk/reward trends on central bank asset allocation and focus on how central banks are leading the green transition.

Finally, we provide an overview of the key takeaways from a discussion held during the central bank peer-to-peer session at the 2024 Amundi World Investment Forum, attended by over 10 central banks and other sovereign entities from around the globe.

2. Do you still see a growing appeal of gold in asset allocation and in other economic roles?

Yes, we believe that gold could be seen as an island of stability in a sea of uncertainty. Determining whether it remains appealing gets us back to the multiple roles of gold – as a currency, a commodity, an investment asset, a luxury consumption good, and an industrial material.

As a commodity, gold appears expensive, particularly compared to other precious metals. It seems pricey relative to traditional macroeconomic drivers, but not against uncertainty, which makes it fairly priced as an investment asset.

As a consumer and industrial good, gold looks expensive against income or wealth per capita, but cheap against golduser- intensive tech companies. Finally, gold looks very cheap as a currency. Most public liabilities are not backed by tangible assets; instead, they rely on public and market trust, as well as the soundness of economic policies. In the United States, for instance, every ounce of gold now backs $138,000 of public debt compared to less than $500 before the collapse of Bretton Woods. Therefore, the re-rating potential of gold, as a currency, looks significant.

We estimate that global investors currently allocate about 2% of their portfolios to gold, amounting to approximately $4 trillion. This allocation is substantially below what portfolio optimisation techniques suggest. A potential increase to 3% could provide significant upside potential for gold prices. Investors can gain exposure to gold through various channels, including direct investment in gold bullion, gold ETFs, and shares in gold mining companies, which can serve as an appealing complementary option to traditional gold investments and remain cheap in relative terms.

3. Do you see a rebalancing from US assets into other asset classes? If so, which assets could benefit from this rotation?

US policy uncertainty is making investors cautious, especially on exposure to US assets, but also on exposure to countries and markets that may be hit hard by US tariffs.

We have seen a rotation towards European equities, both from non-residents but also from European investors moving money back from their US investments. This is seen in both active and passive fund strategies and among sectors, where there is added impetus on defence stocks fuelled by the expected fiscal stimulus to increase defence spending.

We have also witnessed inflows to Emerging Markets (EM), which have proved resilient so far this year, while outflows have been very low compared to late last year, partly due to the dollar correction and lower US ten-year rates. Within EM, equity markets have been more resilient, especially in Latin America that is less affected by tariffs. Investors are attracted by valuations in EM, including in local-currency debt markets.

Beyond this rotation currently underway, large changes in the pattern of capital flows will depend on the ability of non-US markets to absorb large flows. Relative to what is currently held in US markets, this capacity to absorb is limited. The overvaluation metric, which has characterised parts of the US market, could soon be an issue for other markets as well. This will act as a limit, unless we see a major correction in US Treasuries, that, in turn, would lead to disorderly and disruptive changes in capital flows and asset prices.

4. What is driving the US Treasury market? Can it still be considered as a safe haven?

The US Treasury market has historically been viewed as a safe haven for investors, but recent developments are prompting a re-evaluation of this status. Several factors are influencing its dynamics, which may impact its reliability as a refuge during economic uncertainty.

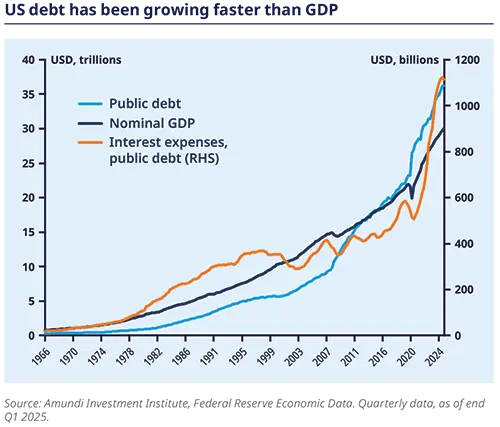

One significant driver is the increasing policy-induced uncertainty stemming from high levels of US debt and lower global growth. With approximately 40% of sovereign debt needing to be refinanced in the next two years, concerns about financial stability are mounting. The recent tariff announcements by President Trump have further rattled markets, leading to volatility in Treasury yields. Initially, yields fell as investors sought safety amid recession fears, but as inflation expectations rose, longerterm yields rebounded sharply.

The supply of US Treasuries is also a critical factor. The United States has been running substantial fiscal deficits since the start of the century: federal debt as a share of GDP has increased from 56% in 2000 to 124% at the end of 2024, leading to higher bond issuance. This growing supply, coupled with declining demand from the Federal Reserve (due to quantitative tightening), should exert upward pressure on yields. If large foreign investors also reduce their holdings, Treasury yields could rise even more relative to swap rates. In the absence of a fall in the swap rate, this could push US nominal yields higher.

Despite these challenges, US Treasuries still hold a unique position in the global financial system. They are considered a benchmark for risk-free assets and play a crucial role in pricing many dollar-denominated securities. The liquidity and stability of the Treasury market make it an appealing option for investors seeking to mitigate risk, especially during periods of market turbulence.

However, the perception of Treasuries as a safe haven may be changing. The recent sell-off in the Treasury market, driven by fears of higher inflation and a deteriorating fiscal outlook, suggests that investors are becoming more cautious. If the market stays under pressure and yields rise due to concerns about credit quality or fiscal sustainability, investors may look elsewhere for safety.

In conclusion, while the US Treasury market is currently facing significant challenges, it retains its status as a key player in global finance. However, the evolving economic landscape and shifting investor sentiment may prompt a re-evaluation of its role as a safe haven in the future. As policy uncertainty persists and global growth slows, the dynamics of the Treasury market will be closely monitored by investors seeking stability in an increasingly complex environment.

5. Do you expect the dollar dominance to fade? And what could be the scope for further FX diversification?

The question of whether dollar dominance will fade is increasingly relevant in today’s economic landscape. While the US dollar has long been the cornerstone of global finance, recent trends suggest a possible gradual shift towards diversification in FX markets.

One indicator of this potential de-dollarisation trend is the rising term premia in US Treasuries and the recent weakness of the dollar. These developments reflect a growing caution among investors regarding US assets in the long term. For instance, the increase in swap spreads and the term premium, particularly at the long end of the yield curve, indicate that investors are becoming more cautious to hold onto US securities. This shift is compounded by the fact that foreign ownership of US dollar assets reached a record $31 trillion in 2024, yet many institutional investors maintain low hedge ratios, suggesting a growing appetite for diversification.

Despite these signs, it is essential to note that de-dollarisation will be a long and complex process. The US dollar still accounts for nearly half of all SWIFT transactions and US equity and bond markets represent the dominant share of global markets. However, as investors increasingly seek to mitigate risks associated with dollar dependency, the scope for FX diversification is expanding.

Emerging markets, particularly India and China, are gaining traction as viable alternatives for investment. The growth gap between emerging and developed markets favours the former, and currencies from these regions may benefit. For instance, the Chinese yuan should remain supported, as policymakers are unlikely to devalue it, given the potential repercussions on international trade relations.

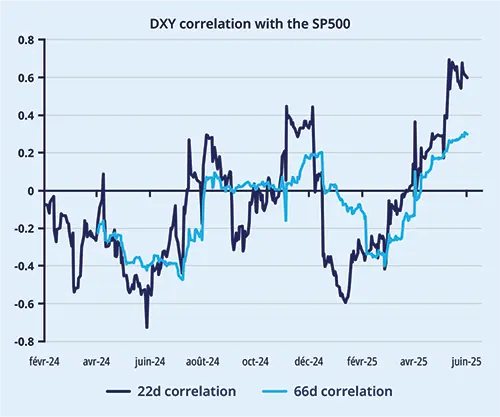

Moreover, the changing correlation structure of the dollar, which now shows a positive correlation with equities, suggests that investors may need to reassess their currency exposure. As the United States faces rising fiscal risks and a potential growth slowdown, the attractiveness of US assets may diminish, prompting a reallocation towards European equities and emerging markets.

In conclusion, while the US dollar is unlikely to lose its dominance overnight, the signs of a gradual shift towards FX diversification are evident, with investors increasingly looking beyond the dollar, exploring opportunities in emerging markets and alternative currencies. This evolving landscape presents both challenges and opportunities for global investors as they navigate the complexities of a changing economic order.

Discover how to ride the policy noise and shifts with

Amundi's Mid-Year Outlook

Find out more on Sovereign entities